Chiffres clés

Vous trouverez en téléchargement les chiffres du financement des entreprises à fin février 2024. Malgré…

Actualités

Vous trouverez en téléchargement la liste des référents AERAS des établissements de crédit.

Communiqués de presse

A l’occasion d’un événement qu’elle organise à Bruxelles, la Fédération bancaire française publie «…

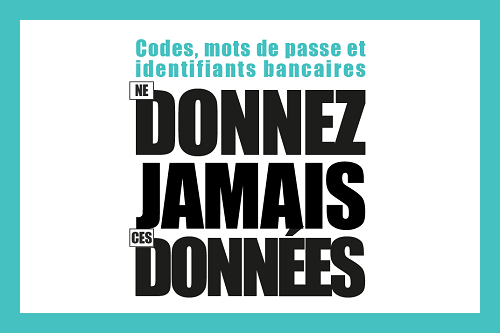

Ne donnez jamais ces données

#VidéoDeLaSemaine

Rapports annuels

Le rapport annuel « L’année de la banque » revient sur les temps forts du secteur bancaire en 2023.Au cœur du financement de l’économie, les banques sont utiles car elles…

Mémos Banque

Parce que nul n’est à l’abri d’un accident de la vie – chômage, séparation, maladie, perte de revenus… – les banques sont à l’écoute de leurs clients afin de les accompagner…

Mémos Banque

Mémo n°5 – la Fédération bancaire française publie un Mémo sur l’Emploi dans les banques.

Autres publications

La Fédération bancaire française publie « La banque, acteur d’un monde durable et responsable », véritable tour d’horizon des réponses apportées par le secteur…

0 document sélectionné